We have identified a more suitable language of this document. To change language to please click here or close

We have identified a more suitable language of this document. To change language to please click here or close

For storing your preferred CMS location, analysing referrals from LinkedIn and embedding third party content we need your consent (which you can withdraw any time).

This website uses cookies so that we can provide you with the best user experience possible. Our Cookie Notice is part of our Privacy Policy and explains in detail how and why we use cookies. To take full advantage of our website, we recommend that you click on “Accept All”. You can change these settings at any time via the button “Update Cookie Preferences” in our Cookie Notice.

Technical cookies (required)

Technical cookies are required for the site to function properly, to be legally compliant and secure. Session cookies only last for the duration of your visit and are deleted from your device when you close your internet browser. Persistent cookies, however, remain and continue functioning on repeat visits.

Analytics

CMS does not use any cookie based Analytics or tracking on our websites; see details here.

Personalisation cookies

Personalisation cookies collect information about your website browsing habits and offer you a personalised user experience based on past visits, your location or browser settings. They also allow you to log in to personalised areas and to access third party tools that may be embedded in our website. Some functionality will not work if you don’t accept these cookies.

Social media cookies

Social Media cookies collect information about you sharing information from our website via social media tools, or analytics to understand your browsing between social media tools or our Social Media campaigns and our own websites. We do this to optimise the mix of channels to provide you with our content. Details concerning the tools in use are in our privacy policy.

1.1.1 In 2002, Albania signed the Athens Memorandum

1

Memorandum of Understanding on the Regional Electricity Market in South East Europe and its Integration into the European Union Internal Electricity Market (signed in Athens on 15 November 2002) D(2002)C2/BD/CA.

and committed, with the other south eastern European countries, to establish an integrated regional electricity market in south-east Europe and to ensure its integration into the European Union’s internal electricity market. This was to be achieved through the introduction of compatible national electricity market models, in line with the First Energy Package. Albania was also a party to the subsequent Athens Memorandum

2

Memorandum of understanding on the Regional Energy Market in South East Europe and its integration in the European Community Internal Energy Market (signed in Athens on 8 December 2003).

, signed in 2003, which eventually led to Albania being a party to the Treaty establishing the Energy Community

3

establishing the Energy Community (adopted 25 October 2005; in force on 1 July 2006) OJ L198/29.(Energy Community Treaty), signed in 2005. The Energy Community Treaty was entered into between the European Union and all the south eastern European countries, including Albania and Kosovo, and established a common regulatory framework. In addition, Albania is a signatory to the Kyoto Protocol (since 2005) and the Stabilisation and Association Agreement (since 2006).

1.1.2 The Albanian electricity power market follows the electricity market model approved by Decision no. 338/2008 of the Council of Ministers

4

Electricity Market Model 2008, Decision of the Council of Ministers (Electricity Market Model). This model aims to implement the Second Energy Package, and the requirements of the Energy Community Treaty, to develop a simple, regulated, transparent and balanced regional electric power market that is attractive to foreign and domestic investors.

1.2 Structure of electricity market

1.2.1 During 2001, the Albanian Energy Corporation (KESH) underwent structural changes, resulting in the establishment of three vertically integrated state-owned entities for generation, transmission and distribution respectively. Previously, KESH was exclusively responsible for generating, transmitting and distributing electricity to customers as well as exchanges with neighbouring countries.

1.2.2 Public electricity generation is carried out by the joint stock company KESH-Gen Sh.A., owned by the government and TEC-Vlorë Sh.A., a wholly owned subsidiary of KESH. KESH has a total installed capacity of 1,531MW for public electricity generation. In 2012, total net generation of electricity for both companies was 4,027,012m kilowatts per hour

5

Albania Energy Regulatory, Annual Report for the year 2012, February 2012, pg. 23.

.

1.2.3 Private electricity generation is carried out by 68 small and medium hydro generating stations (HPPs) through concessions granted to 40 private companies. Following open tender procedures, the government of Albania signed concession agreements with private companies, for a maximum term of 30 years, to build, operate and transfer new HPPs in major rivers. Once installed, the HPPs’ capacity will be equal to 195.8MW, 120MW of which was put into operation prior to the end of 2012. In 2012, the total electricity generated by private companies was 299.9GWh or 7% of the country’s generation

6

Albania Energy Regulatory, Annual Report for the year 2012, February 2012, pg. 31.

.

1.2.4 The transmission and distribution divisions were unbundled from KESH in 2004 and 2007 respectively, giving rise to Transmission System Operator Sh.A (TSO) and the distribution system operator (DSO), Cez Shpërndarje Sh.A. In 2009, the Ministry of Economy, Trade and Energy (METE), on behalf of the government, sold 76% of the shares it held in the DSO to the CEZ Group, an international investor. After four years, this privatisation was considered unsuccessful and, in January 2013, Albania’s Energy Regulatory Authority (Authority) revoked CEZ Shpërndarje’s distribution licence, holding the Czech Group liable for damages for failing to purchase sufficient electricity for the distribution system and not investing in the power grid. The government now administers the DSO

7

Albania Energy Regulatory, Decision no. 4 dated 21 January 2013 (accessed 13 November 2014)

www.ere.gov.al/doc/VENDIM_NR.4_2013.pdf

.

1.2.5 The Electricity Market Model governs the sale and purchase of electric power between market players. Based on this model, the Authority developed and approved market rules and technical and commercial codes that facilitate power purchase agreements between small power producers (SPPs), which are connected to the distribution network, independent power producers (IPPs), which are connected to the transmission network, and various electricity suppliers.

1.2.6 The electricity supply market has been liberalised since 2008, with the issuance of the Energy Law, the Electricity Market Model and the Authority’s energy market rules (Albanian Market Rules), allowing end customers to freely choose their electricity provider based on current market conditions.

1.3 Key players

1.3.1 KESH Gen Sh.A is the dominant electricity generator, providing approximately 98% of the public electricity generated in Albania.

1.3.2 OST Sh.A is the sole owner and operator of the transmission grid. It was unbundled from KESH, giving rise to the TSO in 2004.

1.3.3 Cez Shpërndarje Sh.A. is the dominant DSO and was unbundled from KESH in 2007.

1.3.4 Other market participants include electricity traders, generators, the market operator and end customers.

1.4 Current issues and drivers

1.4.1 The Albanian energy sector is being privatised and the government is determined to solve the country’s energy problems by granting concessions for the construction and operation of small, medium and large HPPs on all major rivers.

1.4.2 Albania is working towards a reliable and sustainable energy sector. Its development will be based on utilising all energy options to meet demand and to create added value for Albanian citizens, in alignment with policies on environmental, economic and social responsibility.

1.4.3 The Energy Sector Strategy for 2006 to 2020 (Energy Strategy)8AKBN – Albanian National Agency of Natural Resources, Energy Sector Strategy (Strategjia sektoriale e energjisë 2006-2020), year of publication 2006, (accessed on 13 November 2014)recommends following an active scenario, which provides a quantitative description of the measures needed to increase efficiency and introduce alternative sources of energy. The Energy Strategy is part of a national general strategy for the economic development of Albania.

1.4.4 The difficult conditions that the country faced for a relatively long period of time, as well as the increased prices of oil, gas and other energy sources on the international market, led to the creation of important objectives for the METE’s energy policy. These include:

strengthening the reliability of energy supply by making effective use of existing energy sources, building new generating stations, diversifying energy supply and connecting the country to regional electricity networks and oil and gas pipelines;

increasing the efficient use of energy by ensuring the lowest possible impact on the environment, which could render the energy sector a supporting sector for the sustainable development of all other economic and social sectors;

establishing an effective institutional framework in line with EU standards and international agreements;

orientating the energy system towards the customer and optimising the energy supply;

liberalising the oil products market and improving the state’s regulatory role in this regard;

encouraging the use of renewable energy sources (including solar, hydro, wind and biomass) to ensure the maximum use of local energy sources; and

establishing an attractive environment for foreign investors to enable, through modern technologies and techniques, the efficient utilisation of internal energy sources and increase domestic generation.

1.4.5 On 5 June 2013, the Renewables Law

9

Për burimet e energjisë së rinovueshme 2013, law no. 138/2013.

entered into full force to comply with all requirements of Directives 2001/77

10

European Parliament and the Council Directive (EC) 2001/77 on the promotion of electricity produced from renewable energy sources in the internal electricity market.

, 2003/30

11

the Council Directive (EC) 2003/30 on the promotion of the use of biofuels or other renewable fuels for transport.

, and 2009/28

12

European Parliament and the Council Directive (EC) 2009/28 on the promotion of the use of energy from renewable sources and amending and subsequently repealing Directives 2001/77/EC and 2003/30/EC

. Furthermore, in April 2012, the National Renewable Energy Action Plan was published, with approval pending from the Council of Ministers.

2. Sector analysis

2.1 Generation

Structure of generation sector

2.1.1 KESH is the state owned generation company. Power may also be generated by SPPs or IPPs who have been granted concessionary rights to exploit renewable energy sources in Albania. The Power Sector Law

13

Për sektorin e energjisë elektrike 2003, law no. 9072/2003.(Energy Law) requires KESH to buy electricity generated by SPPs and IPPs.

2.1.2 Pursuant to section 39 of the Energy Law, the Albanian government encourages generation of renewable energy by IPPs through a system of incentives. An IPP with an installed capacity of more than 50MW using non-renewable sources must produce and/or inject into the transmission system a quantity of renewable energy equal to at least 3% of the energy generated in the previous year from generating stations using renewable sources and certified by the Authority with green certificates.

2.1.3 This obligation is deemed to be fulfilled if an IPP using non-renewable sources purchases the relevant quantity of electricity from renewable energy generators, provided that the Authority, and the corresponding foreign agencies reciprocally (if imported), recognise the certification of the energy produced from the renewable source.

2.1.4 The Albanian government further encourages the construction of renewable energy plants by providing a feed-in tariff for SPPs with an installed capacity up to 10MW. The Energy Law provides for the Authority to indicate a unique price (the feed-in tariff) for electricity generated by such SPPs. In such case, generators are prioritised by the TSO when dispatching the generated electricity.

2.1.5 KESH, based on the tariffs suggested by the Authority, enters into long term agreements with generators to purchase their entire power generation.

2.1.6 Albania has great hydropower potential due to its geographical landscape. Data shows that the annual combined water flow of Albanian rivers is approximately equal to 40b cubic metres which could generate from 16 to 18TWh year.

2.1.7 The Energy Law guarantees new energy generators the ability to access, and connect to, the transmission or distribution systems. New energy generators enter into connection agreements with the TSO/DSO (who are obliged to guarantee access) to transmit/distribute the energy generated into the transmission/distribution system. These connection agreements set out the tariffs and profits of the parties involved.

2.1.8 There are several important HPPs. Fierzë, Koman and Vau i Dejës are under the state’s exclusive ownership and are operated by KESH. Following an international tender in December 2012, Kurum International purchased Ulëz, Shkopet, Bistrica-1 and Bistrica-2.

2.1.9 68 small and medium HPPs are active under generating licences held by private companies. See paragraph 1.2.3 for further details.

Energy Mix

2.1.10 In 2011, HPPs contributed 98% of public electricity production, with thermal generating stations contributing the remaining 2%. In 2012, hydro generating stations accounted for 100% of public electricity production.

2.1.11 The major generation projects, either under construction or already committed to by the Albanian government, are

14

Coordination of Research Polices with the Western Balkan Countries, National background report on energy for Albania, March 2012.

:

Large HPPs (more than 15MW):

VERBUND (Austria), as concessionaire of Ashta HPP, for installed capacity of 48MW in the Drin River (2009-2012) (EUR 160m privately funded);

a consortium of BEG (Italy) and DBank (Germany), as concessionaire of Kalivaci HPP, for installed capacity of 93MW in Vjosa River (2008-2012) (EUR 120m privately funded);

a consortium of EVN (Austria) and Statkraft (Norway), as concessionaire of Devoll River Cascade, for two HPPs Banja and Moglicë, to be built in the valley of Devoll, with an installed capacity of 256 MW

15

Devolli Hydropower website

(2009-2015) (EUR 930m). On March 2013 the Norwegian Statkraft AS signed an agreement by which Statkraft acquired the Austrian EVN AG 50 percent stake in Devoll Hydropower ShA ; and

Kürüm International, for the purchase of four HPPs, two situated in the Mat River (Ulëz – 25.2MW installed capacity, and Shkopet – 24MW installed capacity) and two situated in the Bistrica River (Bistrica 1 – 22.5MW installed capacity, and Bistrica 2 – 5MW installed capacity) (2012) (total price of EUR 110m);

Medium and small HPPs (less than 15MW):

The Albanian government signed concession agreements with 40 private companies to build 68 new facilities (see paragraph 1.2.3);

Thermal generating stations:

Vlora (distillate oil, 97MW, EUR 92m, publicly funded) is financed by a consortium of the European Bank for Reconstruction and Development, the European Bank for Investment, the World Bank and KESH. The plan was for operations to commence in June 2010 but, due to technical problems during the testing process, it has been delayed; and

Lezha (palm oil, 140MW, EUR 150m, privately funded) to be constructed by Marseglia Group (Italy);

Wind generating stations:

Lezha (108 + 114MW) to be constructed by Marseglia Group (Italy); and

A project in Karaburun Vlora (500MW) to be constructed by Moncada Energy Group (Italy).

2.1.12 In the last few years, Albania has faced difficulties in supplying electricity to its citizens. This has been due to a combination of factors, including:

lack of primary energy sources;

lack of interconnected gas networks;

high levels of electricity loss;

limited production and interconnection capacities; and

high electricity consumption for heating.

2.1.13 Until 1998, Albania was a net exporter of electricity. However, demand is now much higher than domestic generation, forcing Albania to be heavily dependent on imports (through KESH).

2.2 Transmission

Structure of transmission sector

2.2.1 Pursuant to the Albanian Market Rules, the TSO, licensed by the Authority, is responsible for transmitting electricity. The transmission system operates at 110-400kV and is owned by the TSO. The TSO has an obligation to properly maintain the electricity lines and connections (national and international). In addition, the TSO must guarantee system’s capacity to meet the domestic demand.

2.2.2 The connection of generators to the transmission and distribution systems is regulated by the Energy Law and relevant secondary legislation, such as the Albanian Market Rules. A generator wishing to participate in the energy market is required to submit a written request to the TSO, who will decide whether or not to enter into a detailed connection agreement. The agreement determines the obligations of the parties, including the payment of charges, and establishes relevant deadlines. Such agreements must be approved by the Authority.

2.2.3 HPPs are also required to submit a registration form to the TSO for entry in the Energy Market Register. Electricity market participants must be registered with the Energy Market Register in compliance with the Albanian Market Rules. The Energy Market Register is a database which holds the identification data, addresses and contact details of each market participant. The registration form contains the following:

name of applicant;

headquarter address and contact details;

phone, fax, e-mail;

position in the electricity market (generator, supplier, trader);

business registration number;

licence issued by the Authority;

bank account data;

a list of authorised persons to execute documents related to operational performance in the electricity market; and

a list of authorised persons to sign contracts and invoices.

In addition, the following documents must be submitted with the registration form:

a copy of the licence for electricity generation, trade licence or electricity supply licence;

grid access document issued by the TSO and/or DSO, as required; and

a copy of the most recent annual balance sheet certified by the relevant tax authority.

2.2.4 The TSO may decline or approve a request within ten business days after receiving the application.

2.2.5 The TSO is required to upgrade its connections and transmission systems from new renewable energy generating stations in line with the Energy Strategy, the renewable energy action plan and other applicable government policy/regulation.

Cross border issues

2.2.6 Albania is interconnected with the transmission systems of Montenegro, Kosovo and Greece. Any issues relating to interconnection capacity, transmission congestion and trade restrictions are, therefore, very important.

2.2.7 The existing links are:

400kV line from Elbasan (Albania) – Kardia (Greece);

400kV line from Tirane (Albania) – Podgorice (Montenegro);

220kV line from V.Dejes (Albania) – Podgorice (Montenegro); and

220kV line from Fierze (Albania) – Prizren (Kosovo).

2.2.8 The new 400kV interconnection with Kosovo (Tirana 2 – Kosovo B) is in the initial phase of construction (total length of 235km).

2.3 Distribution

Structure of distribution sector

2.3.1 The DSO is licensed by the Authority to distribute electric power under the Energy Law. The DSO’s distribution system consists of cable lines, substations and other facilities such as transformer compartments.

2.3.2 The DSO is required to distribute electricity at medium and low voltage (from 35kV to 40kV) to supply end customers according to the price fixed by the Authority each year.

2.4 Supply

Structure of supply sector

2.4.1 The Authority licensed the DSO to carry out supply activities pursuant to the Energy Law.

2.4.2 The DSO supplies medium and low voltage electricity to end customers at a price which is fixed and regulated by the Authority each year.

2.4.3 As mentioned in paragraph 1.2.6 above, the supply market was liberalised in 2008. The Authority has granted several companies supply licences

16

Enti Rregullator I Energjise website (accessed on 13 November 2014)

.

2.4.4 The Authority aims to approve tariffs according to customer categories to ensure that tariffs reflect the real costs of electricity.

2.4.5 The Energy Law defines qualified customers as those energy customers consuming at least 50m kilowatts per hour annually and connected directly with a high voltage line of 110kV (Qualified Customers). Qualified Customers are supplied by any domestic or foreign suppliers licensed by the Authority to purchase electricity from traders, SPPs or IPPs to supply Qualified Customers (Qualified Suppliers). All other customers are supplied with electricity by the wholesale public supplier (WPS) through the low-voltage lines.

2.5 Energy exchange/trading

Structure of trading market

2.5.1 The main purpose of the Electricity Market Model is the promotion of competition in the wholesale and retail markets for Qualified Customers.

2.5.2 In the market, overseen by the Authority, electricity is traded over-the-counter by direct negotiations between market players, who use the form of contract that best suits their needs. Electricity may also be traded via brokered agreements. Qualified Customers must sign purchase agreements with Qualified Suppliers for their supply.

2.5.3 Pursuant to the Electricity Market Model, the import of electricity is carried out by the WPS within KESH, CEZ Shpërndarje Sh.a and Qualified Suppliers. While WPS imports electricity to meet the needs of end customers, CEZ Shpërndarje imports electricity to add capacity to the distribution system and to meet the demand of Qualified Suppliers.

2.5.4 The WPS has a licence to purchase, at prices regulated by the Authority, all the electricity generated by KESH (from its HPPs and other generation), IPPs, SPPs, Qualified Suppliers and traders. The WPS is required to provide all necessary supplies, including imports, to avoid a shortfall.

2.5.5 The WPS is required to purchase electricity generated from renewable energy sources connected to the distribution network regardless of the installed capacity of generating stations.

2.5.6 According to the 2013 Annual Report issued by the Authority, the net production of power in 2013 was 6,956

17

Albanian Energy Regulator, Annual Report for the year 2013, (accessed on 13 November 2014)

www.ere.gov.al/doc/Raporti_Vjetor_2013_perfundimtar.pdf

.

3. Regulation

3.1 Authorities

3.1.1 The Authority is a public entity and was established in 1995. It operates pursuant to the Energy Law and has obligations to

18

Section 8 of the Energy Law.

:

guarantee and develop the energy market according to the principles of transparency, non-discrimination and free market competition;

ensure continuity and security of electricity supply to end customers;

protect the interests of end customers and provide transparent and reasonable tariffs for the trade of energy to the market players; and

protect the environment and citizens' lives by exercising its authority in licensing and monitoring market operators in the energy sector.

3.1.2 The Authority has as executive body consisting of a board of commissioners as well as technical and managerial staff. The chairman must obtain a majority of votes in the Albanian parliament to be elected and hold office. Each year, the chairman reports to parliament about the energy market’s progress.

3.1.3 The Authority takes collegial decisions, with each decision published in the official gazette to be effective.

3.2 Key legislation

3.2.1 The energy laws of Albania include:

the Energy Law;

competition law

19

Për Konkurrencën 1995, law no. 8044/1995, Official Gazette no 27, 1996.

;

environmental protection law

20

Për mbrojtjen e mjedisit 2011, law no. 10431/2011, Official Gazette no 89, 2011

;

concessions law

21

Për koncesionet dhe partneritetin publik privat 2013, law no. 125/2013, Official Gazette no. 76, 2013.

;

the Electricity Market Model; and

the Albanian Market Rules.

3.3 Regulatory framework

3.3.1 Companies active in the energy market must have a licence issued by the Authority to carry out the following activities:

generation;

transmission;

distribution;

supply of electricity to Qualified Customers (Qualified Suppliers only); or

trade of electricity (a trader requires a licence to trade electricity, except for the sale of electricity to the retail public supplier or end customers, which would be covered by a supply licence).

3.3.2 WPS and the retail public supplier, which is an administrative division functionally and financially divided from the DSO licensed for the activity of electricity supply to end customers also require licences from the Authority. Albanian law does not require an operator who generates electricity for personal needs (i.e. not for sale to third parties) to hold a licence.

3.3.3 Each licence issued by the Authority is for a set term. For example, the term for a generation or distribution licence does not exceed 30 years. Transmission licences granted to the TSO do not exceed 25 years. Trade, distribution, wholesale and retail supply licences are valid for a maximum of 5 years.

3.4 Support schemes

Renewable energy

3.4.1 In 2013, a new law on renewable energy

22

Për burimet e energjisë së rinovueshme 2013, law no. 138/2013, Official Gazette no. 83 dated May 20, 2013.

was introduced to implement Directive 2009/28

23

European Parliament and the Council Directive (EC) 2009/28 on the promotion of the use of energy from renewable sources and amending and subsequently repealing Directives 2001/77/EC and 2003/30/EC

. The law aims to:

increase the diversification of energy resources and provide efficient energy supply in the country;

reduce greenhouse gas emissions and protect the environment in compliance with the country’s international commitments under the UNFCCC

24

United Nations Framework Convention on Climate Change opened for signature on 9 May 1992.

, the Kyoto Protocol and other international treaties; and

promote clean technologies for utilisation of renewable energy sources.

3.4.2 The METE, in cooperation with the Ministry of Environment, drafted the National Renewable Energy Action Plan.

3.4.3 The National Renewable Energy Action Plan still needs to be approved by the Council of Ministers. Once it has been approved and comes into force, the Minister responsible for energy will be required to report to the Council of Ministers each year on its implementation and targets.

3.4.4 The Albanian government will introduce a one-stop-shop licensing centre for power generators using renewable energy sources.

Feed-in tariff

3.4.5 An attractive feed-in tariff is already in place for small hydro-generators, but the government is still in the process of determining the incentive mechanism for encouraging more immediate investment in renewable energy technologies.

Guarantee of origin and green certificates for renewable energy sources

3.4.6 The Energy Law has given the Authority the power to issue guarantees of origin (Green Certificates) for electricity generated by renewable sources.

3.4.7 These guarantees of origin are issued for:

all energy generated from hydro-generators, on an annual basis (less the energy used for pumping reserves);

the annual level of energy generated from biomass, wind, solar and geothermal sources; and

the amount of energy generated in cogeneration systems, if the amount of energy from non-renewable sources does not exceed 5% of the total energy generated.

3.4.8 The issue of Green Certificates requires generating stations that produce renewable energy to be qualified as such by the Authority. The qualification procedure takes up to 90 days.

3.4.9 The Energy Law envisages Green Certificates to be an official document, with a limited time value, that can be transferred or traded separately from the energy generated. A Green Certificate certifies the energy generated from renewable sources or any combined method of green energy. It also identifies the date and place of generation and ownership title.

3.5 Upcoming regulatory changes

3.5.1 One of the biggest challenges facing the future of energy sector development in Albania is dealing with the increase of energy consumption per capita whilst maintaining a low relative level of energy intensity to induce an efficient and competitive economy in an increasingly more open international market. In 2015, the newly elected government expects to introduce reforms in the Albanian energy market. Albania has historically experienced an abnormally high growth rate of electricity consumption. A large part of that growth has been artificially stimulated by extraordinarily high rates of electricity theft, non-payment of electric bills and tariff rates set well below cost. For the past decade, customers have failed to reduce electricity usage or make use of alternative fuels. The artificially high electricity consumption, particularly for space heating, has diverted electricity away from commercial and industrial uses that could otherwise create jobs and contribute to economic growth.

3.5.2 Along with the Albanian renewable strategy, the Albanian investments strategy aims to:

provide a reliable and sustainable energy sector to meet the country’s energy demand;

increase the efficient use of energy;

increase the diversification of energy resources and provide efficient energy supply in the country;

reduce greenhouse gas emissions and protect the environment in compliance with the country’s international commitments under the UNFCCC, Kyoto Protocol and other international treaties;

promote clean technologies for the utilisation of renewable energy sources; and

create an effective regulatory and institutional framework according to EU standards.

4. Country Statistics

4.1 Electricity generation

Figure 1: Generation of electricity in Albania (1985-2011)25Energy Regulatory Authority, Annual Report 2012, February 2012 (accessed on December 4,2014)

www.ere.gov.al/doc/raportivjetor2012.pdf

Figure 2: Generation of electricity from key HPPs in Albania (2005-2011)26Energy Regulatory Authority, Annual Report 2012, February 2012 (accessed on July 18 2013)

www.ere.gov.al/doc/raportivjetor2012.pdf

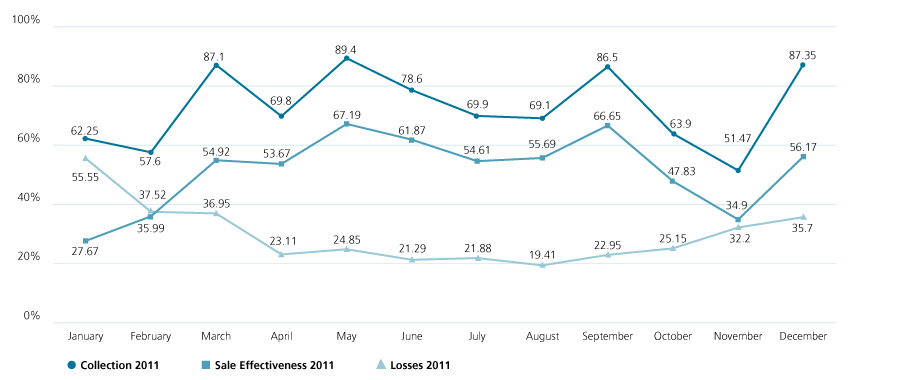

4.2 Collection, losses and sale effectiveness

Figure 3: Collection, losses and sale effectiveness in Albania during 201127Energy Regulatory Authority, Annual Report 2012, February 2012 (accessed on July 18, 2013). Sale effectiveness expresses the final result of efficiency in electricity consumption taking into consideration the common effects for the level of billing and collections.

www.ere.gov.al/doc/raportivjetor2012.pdf

%20(2).jpg?v=3)

Social Media cookies collect information about you sharing information from our website via social media tools, or analytics to understand your browsing between social media tools or our Social Media campaigns and our own websites. We do this to optimise the mix of channels to provide you with our content. Details concerning the tools in use are in our privacy policy.