This Back to Basics note follows our key concepts briefings, which intend to provide high-level insights regarding funds fundamentals, funds vehicles and operational considerations, available here.

In this Back to Basics, we look at UK Real Estate Investment Trusts (“REITs”), including their requirements, benefits and growing use for fund structures and investment by institutional type investors in UK real estate.

Background and relevance

Recent changes in UK tax legislation – most recently in the Finance Act 2024 – as well as changing investor attitudes, have bolstered investor and manager appetite for UK REITs as part of a fund or as holding vehicles (“Private REITs”). They were originally introduced in 2007 for listed companies but can now be more “private” in nature and it is no longer necessary for the REIT to be traded or listed on a recognised stock exchange if the relevant ownership requirements are met.

What is a UK REIT?

A UK REIT is a UK tax resident company limited by shares (or a group of companies of which the principal company is a UK tax resident) that has an HMRC approved tax status for its property rental business and associated investment in real estate assets.

What are the key benefits?

Prominent benefits of using UK Private REITs to hold and invest in UK property include:

- tax efficient structure – see Tax benefits further below;

- use for real estate – this can be single or multi sector asset classes and includes student accommodation, private rented sector and life sciences;

- private REITs can be used by funds and institutional investors – see Private REIT structures below;

- possible use for a single asset – a REIT can hold a single commercial property of £20 million or more; and

- flexibility – a UK REIT can be an overseas entity, provided it is a UK tax resident, and can be a group structure. It can be managed internally or externally. REITs are also permitted to hold non‑UK assets, which will be subject to local taxes, and to carry out a limited amount of non‑real estate investment activity.

REIT requirements

Set out below is a diagram illustrating some of the key “qualifying conditions” of REITs:

There are other conditions such as for financing, maximum holdings of shares by single corporates as well as continuing requirements. If these are not met, a tax charge can arise, or even loss of REIT status.

Tax benefits

A key incentive for using Private REITs is the tax efficiencies that are offered. These efficiencies include:

- no UK corporation tax is payable on tax derived from the property rental business: this has particularly become more favourable for investors following the uplift in main rate corporation tax from 19% to 25% in 2023. It is required to distribute at least 90% of its rental income profits;

- no capital gains tax is payable on profits arising from its property investments: this includes gains on the sale of qualifying UK property rich companies;

- ability to eliminate tax on latent gains: REITs can eliminate latent gains in property holding companies they acquire that hold UK property and can sell such property holding companies free of latent gains. This is highly desirable for purchasers when bidding for property holding companies at a gain;

- tax is levied at the shareholder level than at the REIT level itself: this enables certain institutional investors to claim exemptions on profits received from the property;

- a company acquiring REIT status is not subject to any additional tax charges for becoming a REIT; and

- ability to reclaim withheld tax: while distributions out of its ring-fenced profits (otherwise referred to as property income distributions (“PIDs”)) made by the REIT are subject to a 20% withholding tax, these payments can be made gross where a shareholder is a UK corporate, pension fund, local authority or charity. UK companies will be liable to corporation tax on the PIDs at the current rate of UK corporation tax. Non-resident investors may be eligible to a reduced (or nil) withholding tax rate.

Recent legislative amendments of REIT law

Further changes to the REIT regime have recently been made by successive Finance Acts, with the most recent in the Finance Act 2024.

Many of the recent amendments seek to reduce barriers to entry which we anticipate will heighten investor interest and participation in the REIT regime and create greater flexibility in fund structuring as it can accommodate REIT subsidiaries. These include:

- amending the non-close condition, which applies where a company is only close because it has an institutional investor as a participator, so that it is possible to trace through the intermediate holding companies to an institutional investor which is an ultimate beneficial owner; and

- allowing more fund structures to meet the “genuine diversity of ownership” condition, by allowing the fund structure to be looked at as a whole, rather than just the investing vehicle.

The amendments made in the Finance Act 2024 include a change to the definition of “institutional investors” such that authorised unit trusts, open-ended investment companies and collective investment scheme limited partnerships must meet either:

- a “genuine diversity of ownership” condition (i.e. it is widely marketed) can be fulfilled by looking at the fund structure as a whole rather than just the investing vehicle; or

- a “not a close company” condition (i.e. not controlled by 5 or fewer participators).

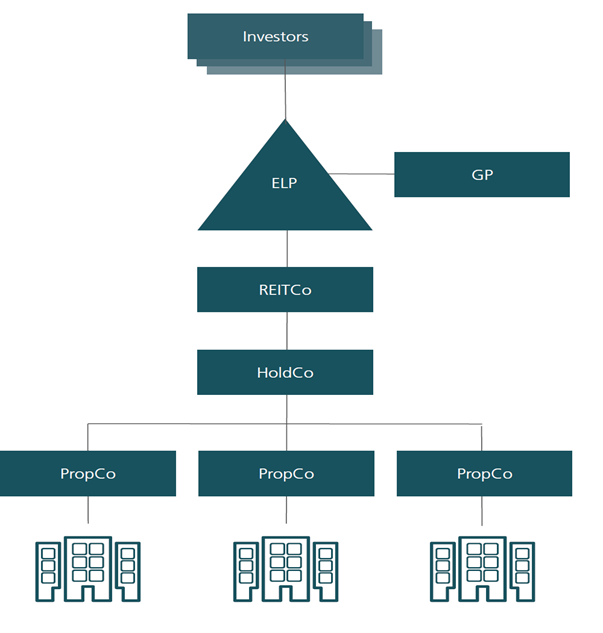

Private REIT structures

It is possible for institutional investors to hold the Private REIT directly or through a fund structure if the relevant investor and other requirements are met (see 70% institutional ownership requirement in the diagram and proposed legislative changes above). Institutional investors include relevant authorised unit trust schemes, pension schemes, sovereign wealth funds, open-ended investment companies, collective investment scheme limited partnerships, other UK REITs (or overseas REIT equivalents), UK charities and certain insurance companies.

Private REITs often do not need a listing or to be traded on a recognised stock exchange.

An example of a UK Private REIT structure set up as a fund is provided below.

Luxembourg vehicles

The new Luxembourg-UK double tax treaty (as explored in our separate briefing (The new Luxembourg-UK double tax treaty: key points for investors in UK real estate (cms-lawnow.com))) with its new taxing right taking effect from 1 January 2024 in respect of withholding tax, and from 6 April 2024 applying to other taxes on income and gains in Luxembourg, is anticipated to have a knock-on effect on how existing UK real estate holdings should be most effectively structured where shares or interests are held by Luxembourg holding structures. This Luxembourg-UK double tax treaty, in conjunction with the UK corporation tax increasing to 25% on 1 April 2023, is expected to propel UK real estate investors further in considering the use of Private REITs in their own structuring.

Conclusion

If you would like to discuss public and private REITs and their usage in funds, joint ventures or other investment structures, please contact a member of the CMS UK Funds Group.

For further information on our REITs expertise, please see our separate brochure (CMS REITs | Corporate | United Kingdom | International law firm CMS).

Social Media cookies collect information about you sharing information from our website via social media tools, or analytics to understand your browsing between social media tools or our Social Media campaigns and our own websites. We do this to optimise the mix of channels to provide you with our content. Details concerning the tools in use are in our privacy policy.