(Last updated: 30 August 2023)

EU DAC 6 Directive – Disclosure requirements for cross-border tax arrangements

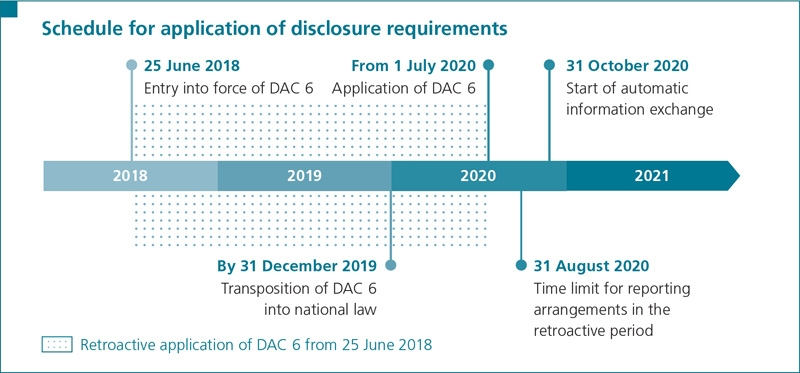

On 25 June 2018, Council Directive (EU) 2018/822 of 25 May 2018 amending the EU Directive on Administrative Cooperation (2011/16/EU) entered into force. Briefly, the Directive – also known as DAC 6 – requires intermediaries (and in some circumstances taxpayers) to report information on certain cross-border tax arrangements to the tax authorities if the arrangements contain specific hallmarks. The objective of these EU-wide disclosure requirements is to combat potentially aggressive tax planning through greater transparency. Member States will be able to identify potentially harmful structures at an earlier stage, with faster adaptation of tax laws helping to prevent erosion of the country’s tax base. Although the focus is on aggressive or potentially aggressive arrangements, the scope of the Directive is very broad and may also trigger disclosure requirements with regard to standard arrangements which are known to be legal and common transactions with a cross-border dimension.

EU Member States were required to transpose DAC 6 into national law with effect from 31 December 2019. The new regulations have been applicable since 1 July 2020. The exchange of information among the EU Member States commenced on 31 October 2020.

Implementation of DAC 6 in Germany

In Germany, the EU Directive was transposed into national law through the Act on the Introduction of an Obligation to Disclose Cross-border Tax Arrangements (German Federal Gazette I 2019, 2875), which was promulgated on 21 December 2019 and entered into force on 1 January 2020. For this purpose, sections 138d to 128k were added to the Fiscal Code (Abgabenordnung – AO).

The (official) interpretation and application of the legislation was accompanied by the German Ministry of Finance (BMF) circular of 29 March 2021. This application circular was amended most recently by the BMF circular dated 23 January 2023. See also here on the website of the German Federal Central Tax Office (BZSt) for an overview of the BMF circulars relevant to DAC 6.

Update: Current draft bill of the "Wachstumschancengesetz" proposes that disclosure requirements should now also include domestic tax arrangements. Although the introduction of disclosure requirements to include domestic tax arrangements was discussed during the transposition of DAC 6, it was rejected during the legislative process. It had nevertheless been expected ever since that disclosure requirements would be extended to include domestic arrangements, as also agreed in the governing parties’ coalition agreement in 2021. This was confirmed by the initial draft of a law to strengthen growth opportunities, investment and innovation, and to promote simplification of taxation as well as tax fairness (Wachstumschancengesetz), which was published on 17 July 2023.In addition to various amendments to the existing regulations on the disclosure requirement in relation to cross-border tax arrangements (sections 138d ff. of the Fiscal Code (AO)), the initial draft proposes an extension of the previously introduced disclosure requirements to include domestic tax arrangements (new sections 138l to n, AO-E). |

The official draft bill published by the government on 30 August includes further changes with regard to some aspects of the planned new rules.

Brief overview of disclosure requirements for cross-border tax arrangements

The material scope of the disclosure requirements essentially includes specific types of tax, the cross-border arrangement, and certain hallmarks of the arrangement:

Type of tax covered

The disclosure requirement for cross-border tax arrangements includes income tax, corporation tax, trade tax, inheritance tax, gift tax and real estate transfer tax, for example. It does not cover (import) VAT, customs duties and harmonised excise duties (such as taxes on energy, electricity, spirits and tobacco), social security contributions and fees.

Cross-border nature of the arrangement

DAC 6 stipulates that arrangements are subject to disclosure if certain cross-border criteria are met, such as more than one EU Member State being involved or, under certain circumstances, at least one Member State and one or more third countries.

Hallmarks of the arrangement – overview

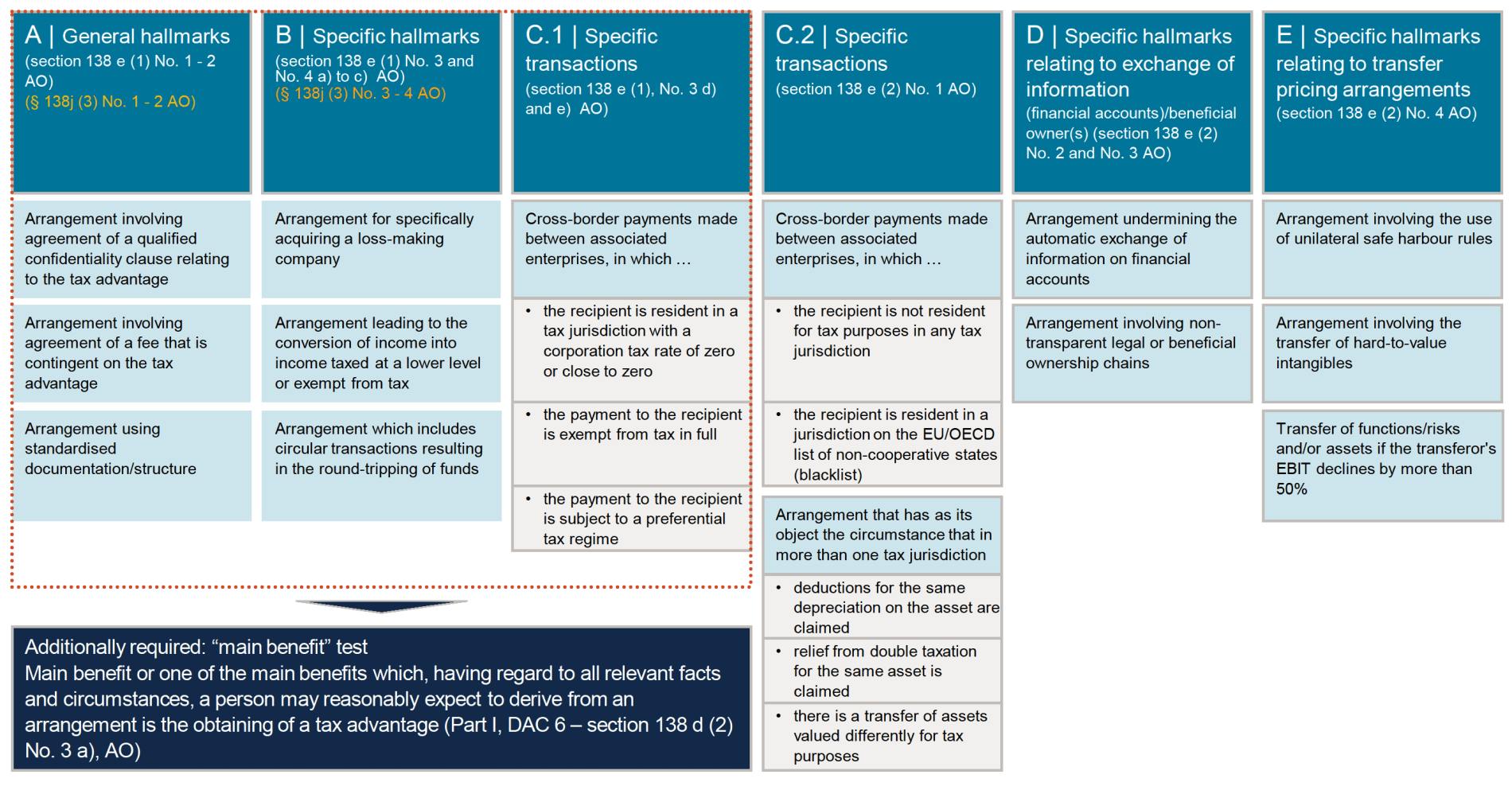

A cross-border arrangement is reportable if it includes at least one specific hallmark within the meaning of DAC 6. With regard to the hallmarks of an arrangement, a distinction must be made between hallmarks which are subject to disclosure irrespective of any tax advantage provided by the arrangement, and hallmarks which only apply if the “main benefit” test is satisfied. This relevance test is regarded as largely satisfied if the expected main advantage or one of the main advantages of the arrangement is the obtaining of a tax benefit.

Overview of hallmarks for the disclosure requirement in relation to cross-border tax arrangements: DAC 6 hallmarks as defined in Annex IV Part II Category A-E; trans-posed by section 138e of the Fiscal Code (Abgabenordnung – AO) in the version that entered into force on 1 January 2020.

Who does the disclosure requirement for tax arrangements apply to?

The disclosure requirement for cross-border tax arrangements mainly applies to intermediaries. According to the legal definition provided, this means primarily any person who designs, markets, organises or makes available for use a reportable cross-border tax arrangement, or who manages its implementation by third parties.

The disclosure requirement is linked to involvement in the various stages of tax planning, from its origin through to implementation. Having said that, someone who has only been involved in implementing individual partial steps of a cross-border tax arrangement without knowing it and without reasonably being expected to know it, will not be regarded as an intermediary, according to the explanatory notes.

Classification as an intermediary does not depend on belonging to a particular professional group. In addition to members of the legal, tax and auditing professions, in practice financial services providers such as banks, fund initiators and insurance companies as well as asset and investment advisors including family offices may be affected by the disclosure requirements. In addition, group financing companies in particular may also be subject to disclosure requirements.

The intermediary must also be linked to EU jurisdiction, e.g. by being domiciled in an EU Member State or by operating a permanent establishment in a Member State, through which services are provided for the arrangement in question. If the intermediary has a specific domestic connection to Germany (e.g. is domiciled in Germany), it is accordingly also subject to reporting requirements in Germany.

Note: A tax arrangement may also be subject to reporting requirements in more than one EU Member State if an intermediary has a domestic connection in more than one EU Member State, or if several intermediaries with different domestic connections are involved in the arrangement. With regard to the disclosure requirement of a (domestic) intermediary, it is also irrelevant whether Germany itself is affected by the cross-border tax arrangement or whether the effects occur solely outside the country.

Users (taxpayers)

If there is no intermediary subject to disclosure requirements, for example, or if the intermediary is (partially) exempt from disclosure requirements due to professional secrecy obligations, e.g. in the case of lawyers, tax advisors and auditors, the users (taxpayers) of the tax arrangement may be subject to disclosure requirements under certain circumstances. A user is considered to be any person to whom a reportable cross-border arrangement is made available for implementation, or who is ready to implement an arrangement of this type or has implemented the first step of such an arrangement.

Specifically, in the case of cross-border tax arrangements that a user designs for their own use (in-house arrangements), the rules applicable to intermediaries apply accordingly. In this case, the user is subject to an independent disclosure requirement. In other EU Member States, the user may have to ensure that the intermediary complies with its disclosure obligations, otherwise the disclosure requirement may revert to the user.

How and when are disclosure obligations to be fulfilled?

The disclosure obligations under DAC 6 generally apply from 1 July 2020. Intermediaries or users must comply with their disclosure obligation within 30 days after the occurrence of the reportable event (in practice, it may be difficult to establish this date precisely). They must submit the information electronically to the German Federal Central Tax Office (BZSt), using the officially prescribed data record.

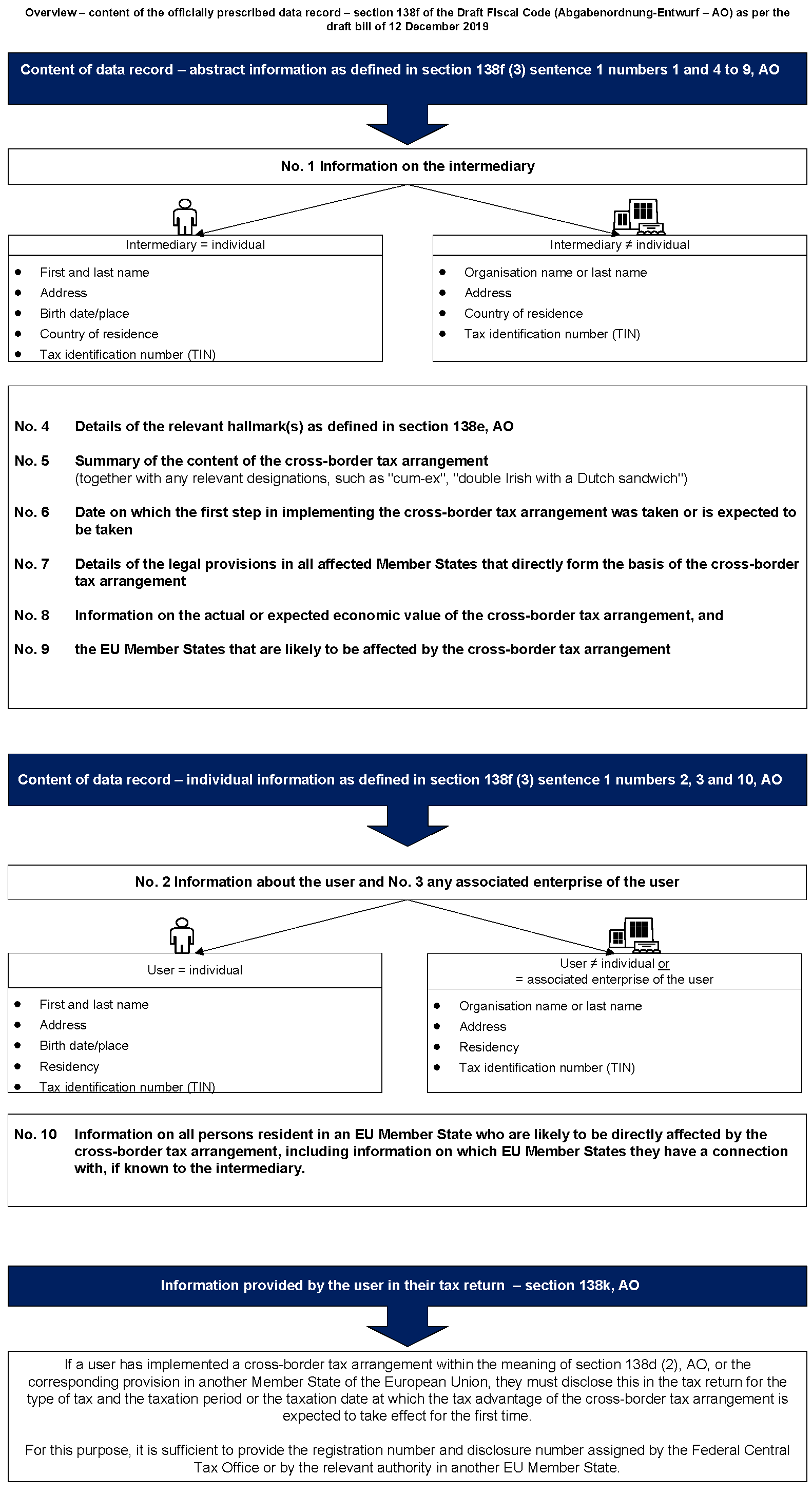

What data must be disclosed?

In addition to abstract information about the intermediary, the relevant hallmarks and the content of the arrangement, the data record must also contain individual information about the user and the other persons concerned, as well as the date of implementation. The details are laid down in the principal procedural regulations, section 138f and section 138g of the Fiscal Code (AO), for intermediaries and users.

Reportable data at a glance

For each data record received, the Federal Central Tax Office (BZSt) will assign a registration number ("ArrangementID") to the cross-border tax arrangement and a disclosure number for the report received ("DisclosureID"). The intermediary must also inform the user of these numbers. One of the reasons for this is that the user is required to indicate in their tax return that a cross-border tax arrangement has been implemented; to do so, the user must state the registration and disclosure numbers.

In the event that the intermediary is subject to a statutory (i.e. not a contractual) obligation to maintain confidentiality, without having been released from this obligation by the user, intermediaries can be exempted from disclosure requirements in certain circumstances. In Germany, however, this exemption has been implemented only in part. This means that with regard to the "abstract information" (numbers 1 and 4 to 9), the intermediary always remains subject to disclosure requirements, even if under an obligation to maintain confidentiality. In these cases, however, the intermediary’s disclosure requirement can be met by the user providing this information on behalf of the intermediary (i.e. by submitting just one data record). Only the requirement to disclose the individual information (numbers 2, 3 and 10) may pass to the user if the intermediary has informed the user in advance about the option of exemption from the obligation to maintain confidentiality and the transfer of the disclosure requirement, and has provided the user with the necessary information specified in numbers 2, 3 and 10 as well as the registration and disclosure numbers, insofar as the user is not aware of this information.

Other special aspects also need to be taken into account, e.g. in scenarios in which at least one other intermediary is subject to a requirement to disclose the same cross-border tax arrangement within the scope of this legislation or in another Member State of the European Union.

Penalties for breaching disclosure requirements

If a reportable cross-border arrangement is not reported, incorrectly reported, incompletely reported or reported too late, fines of up to EUR 25,000 may be imposed for each single breach.

In addition to disputes with the tax authorities, professional advisors could easily suffer reputational damage. Even given compliance with the disclosure requirements, there is thus a strong case for intermediaries to have an agreed communication strategy in place with regard to the tax arrangements as part of a commitment to corporate social responsibility.

Disclosure requirements for tax arrangements – what are your responsibilities?

More than two years after DAC 6 came into force, intermediaries affected by the legislation are still facing legal and administrative challenges as a result of the complex disclosure requirements. The upcoming extension of disclosure requirements to cover domestic tax arrangements will exacerbate the existing situation in terms of the complexity of the tasks involved. When dealing with disclosure obligations, the following aspects will be paramount in cross-border scenarios, and in future also in domestic arrangements:

- Identification of all potentially reportable arrangements in which you are involved as an intermediary.

- Collection of relevant data on potentially reportable arrangements, as well as documenting the results of both reportable and non-reportable arrangements.

- Identification of and coordination with other intermediaries involved, including determining whether the disclosure by the other intermediary has actually been made (requirement of proof of exemption from disclosure requirement for the arrangement).

- Making the disclosure and informing the taxpayer (user) that disclosure has taken place.

- Establishment of efficient internal processes for identification, analysis and documentation of reportable arrangements as part of a functioning compliance management system. This requires the definition of clear lines of responsibility and communication. It should be noted that setting up and configuring an IT-supported reporting system may take several months in some cases.

- Provision of key information (kick-off event) and regular training courses for responsible employees on all matters relating to disclosure obligations.

How can CMS support you?

We are available to provide expert assistance around developing individual solutions to meet your disclosure obligations, both in Germany and across the international CMS organisation.

Our services are carefully tailored to your requirements and include:

Detailed analysis

- Assessing the impact of the disclosure requirements on your company, including analysis of your business models

- Specific analysis of individual arrangements and products with regard to any disclosure requirement

- Systematic support for identifying, assessing, documenting and notifying reportable tax arrangements

Help with self-help

- Training employees on their disclosure duties and assessing disclosure responsibilities

- Advice around designing and introducing compliance management systems that meet MDR criteria and protect against penalties in the event that disclosure requirements are breached

CMS worldwide

- Coordination with international CMS offices in the case of disclosure requirements in other/multiple EU Member States

- Local representation in disputes with tax authorities, including in other EU Member States

Social Media cookies collect information about you sharing information from our website via social media tools, or analytics to understand your browsing between social media tools or our Social Media campaigns and our own websites. We do this to optimise the mix of channels to provide you with our content. Details concerning the tools in use are in our privacy policy.